Commercial Banks (CBs), as a significant part of the Banking System in India, play a pivotal role in the Indian financial sector. They are the backbone of the economy, providing the financial resources necessary for growth and development. This article of NEXT IAS aims to study Commercial Banks (CBs) in detail, including their classification, types, roles & significance, and other related concepts.

As per the current structure of Commerical Banks in India, they are divided into two categories:

SCBs refer to those Commercial Banks under the Banking System in India that are listed in the 2nd Schedule of the Reserve Bank of India Act, 1934 (RBI Act, 1934).

NSCBs refer to those that don’t meet the criteria to be included in the 2nd Schedule of the Reserve Bank of India Act, 1934 (RBI Act, 1934). Being excluded from the schedule means they operate under a different set of regulations as compared to SCBs.

| Basis of Difference | Scheduled Commercial Banks (SCBs) | Non-Scheduled Commercial Banks (NSBCs) |

|---|---|---|

| Meaning | Listed in the second schedule of the RBI Act 1934. | Not mentioned in the second schedule of the RBI Act 1934. |

| Criteria | – Should have a paid-up capital of `5 lakhs or more. – Have to ensure that its affairs are not conducted in a manner detrimental to the interest of its depositors. | – No fixed criteria as such. |

| Regulatory Requirements | – Have to keep CRR deposits with the Reserve Bank of India. – Required to file their returns on a periodic basis. | – Have to maintain CRR deposits with themselves. – No requirements for filing returns as such. |

| Rights Available | – Authorized to borrow funds from the RBI. – Can apply to join the clearinghouse. – Can avail of the facility of rediscount of first-class exchange bills from RBI. | – Usually, not authorized to borrow funds from the RBI. However, they can borrow from the RBI under emergency conditions. – Not eligible for membership in the clearinghouse. – Facility of rediscounting exchange bills from RBI is not available for them. |

| Risk | – They are financially stable and are unlikely to hurt the rights of the depositors. | – These banks are riskier to do business. |

| Examples | – Most of the Commercial Banks under the Banking System in India are SCBs. For example, State Bank of India (SBI), HDFC Bank, etc. | – As of now, there are no NSCB under the Banking System in India. |

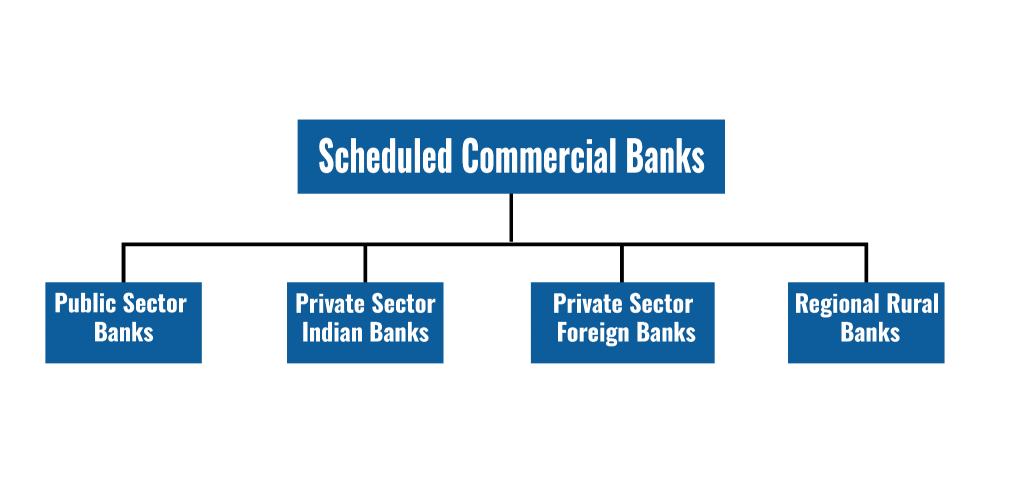

There are various types of SCBs in India, as can be seen as follows.

| Types of Scheduled Commercial Banks (SCBs) | Majority Shareholder(s) | Example(s) |

|---|---|---|

| Public Sector Banks (PSBs) | Government of India | SBI, PNB, Canara Bank, Bank of Baroda, Bank of India, etc. |

| Private Sector Banks | Private Individuals | ICICI Bank, HDFC Bank, Axis Bank, Kotak Mahindra Bank, Yes Bank etc. |

| Foreign Banks | Foreign Entities | Standard Chartered Bank, Citi Bank, HSBC, Deutsche Bank, BNP Paribas, etc. |

| Regional Rural Banks (RRBs) | Central Government, Concerned State Government, and Sponsor Bank in the ratio of 50:15:35 | Andhra Pradesh Grameena Vikas Bank, Uttranchal Gramin Bank, Prathama Bank, etc. |

| List of Public Sector Banks (PSBs) or Nationalized Banks in India |

| – State Bank of India (SBI) – Punjab National Bank (PNB) – Bank of Baroda (BoB) – Canara Bank – Central Bank of India – Indian Overseas Bank (IOB) – Union Bank of India (UBI) – Indian Bank – Bank of India – Punjab & Sind Bank – UCO Bank – Bank of Maharashtra |

| Note: – Oriental Bank of Commerce and the United Bank of India have been merged with Punjab National Bank. – Dena Bank and Vijaya Bank have been merged with the Bank of Baroda. |

These are banks under the Banking System in India that were left out of the nationalization process (in 1969 and 1980) due to their small size and regional focus.

These are banks in the Indian Banking System that came into existence after 1991 with the introduction of economic reforms and financial sector reforms. After the adoption of LPG reforms in 1991, the Banking Regulation Act was amended in 1993. It allowed the entry of New Private Sector Banks in the Banking System in India.

Foreign Banks refer to those banks that have their headquarters in a different country but operate branches or subsidiaries within India. For example, HSBC, Citi Bank, etc.

Commercial Banks in India perform several critical functions in the Indian Financial System, which makes them significant for the Indian economy. Some of their crucial functions and significance can be seen as follows:

Various types of Commercial Banks in India not only support economic growth but also play a significant role in social transformation by promoting financial inclusion. As they continue to evolve, these institutions will remain central to the economic narrative of India, driving future development and fostering a more inclusive economic environment.

They are those banks under the Banking System in India that run on a commercial basis and operate to earn a profit.

They are of, broadly, two categories – Scheduled and Non-Scheduled. While there is no major Non-Schedule Commercial Bank in India, there are various types of Scheduled Commercial Banks viz – Public Sector Banks (PSBs), Private Sector Indian Banks, Private Sector Foreign Banks, and Regional Rural Banks (RRBs).

Based on the branch network and loan portfolio, the State Bank of India (SBI) is the largest Commercial Bank in India.